hullo,good afternoon, on this occasion will be discussed aboutinsurance fraud detection market Insurance Fraud Detection Market Size, Trends & Services - 2024 see more.

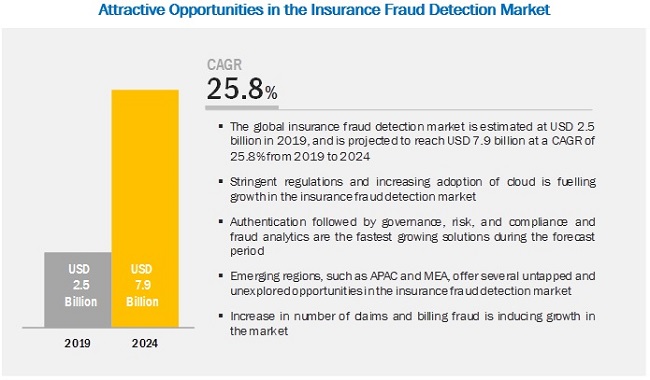

[155 Pages Report] The insurance fraud diagnosis mart expected to fill out from USD 2.5 billion in 2019 to USD 7.9 billion via 2024, at a Compound Annual Growth Rate (CAGR) of 25.8% throughout the anticipate period. The major factors forceful the growth of the mart are the need to run huge volumes of identities via organizations effectively; improving working efficiency & enhancing the consumer experience; increasing adoption of advanced analytics techniques; including stringent regulatory compliances.

The fraud analytics segment to constitute the largest mart extent throughout the anticipate period

The Small including Medium-sized Enterprises (SMEs) segment is expected to fill out at a higher CAGR throughout the anticipate time

The SMEs segment is expected to fill out at a higher CAGR throughout the anticipate period, owing to the increasing incidences of insurance frauds including cyber attacks on top of SMEs. The SMEs are small in terms of their extent but cater to a large number of customers globally. Robust including comprehensive security solutions are not implemented in SMEs expected to financial constraints. However, the large enterprise segment is estimated to keep a higher mart share in 2019.

Insurance fraud diagnosis solutions including services own been deployed over on-premises including cloud environment. Cloud stationing is expected to fill out at the highest CAGR throughout the anticipate period, while the on-premises stationing way is estimated to keep the largest Insurance Fraud Detection Market extent in 2019.

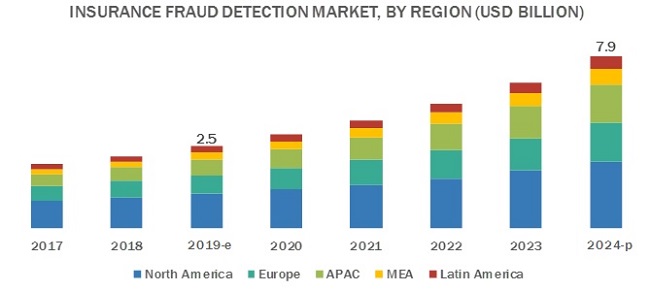

North America to account for the largest mart extent throughout the anticipate period

The global insurance fraud diagnosis mart has been segmented based on top of regions into North America, Europe, Asia Pacific (APAC), Middle East & Africa (MEA), including Latin America to give a region-specific study in the report. North America, followed via Europe, is estimated to become the largest revenue-generating area for insurance fraud diagnosis solution including system vendors in 2019. Trends such when the Internet of Things (IoT), cloud adoption, including Bring Your Own Device (BYOD); including growing internal & external threats are some of the opener factors expected to petrol the growth of the mart in North America.

The APAC mart is gaining traction, when the number of smart devices including BYOD trend are increasing in the developed including developing nations in APAC. The SMEs, when well when large enterprises in APAC, are becoming increasingly aware of the rising instances claims fraud, identity thefts, remittance frauds, including own now started adopting insurance fraud diagnosis solutions including services to combat them.

Key Insurance Fraud Detection Market Players

Major vendors that offer insurance fraud diagnosis services across the globe are FICO (US), IBM (US), BAE Systems (UK), SAS Institute (US), Experian (Ireland), LexisNexis (US), iovation (US), FRISS (Netherlands), SAP (Germany), Fiserv (US), ACI Worldwide (US), Simility (US), Kount (US), Software AG (Germany), BRIDGEi2i Analytics Solutions (India), including Perceptiviti (India). These vendors own adopted opposed types of organic including inorganic growth strategies, such when recent product launches, partnerships including collaborations, including acquisitions, to expand their offerings in the market.

FRISS (Netherlands) is acknowledged when one of the principal vendors in the insurance fraud diagnosis market. To maintain its principal position, the business focuses on top of understanding the fast-changing needs of its clients including has adopted effective growth strategies to enhance its offerings including extend its mart reach. For expanding its footprint, FRISS partnered accompanied by EVRY, to give Fraud Detection when a Service in the Nordics region. The business has implemented different strategies to deliver cutting-edge insurance fraud diagnosis to global organizations. Various organic including inorganic growth strategies are helping insurance fraud diagnosis vendors to stay ahead in the global insurance fraud diagnosis industry.

Scope of the Report

|

Report Metric |

Details |

|

Market extent available for years |

2017–2024 |

|

Base year considered |

2018 |

|

Forecast period |

2019–2024 |

|

Forecast units |

Value (USD Million) |

|

Segments covered |

Component, stationing type, company size, including region |

|

Geographies covered |

North America, Europe, APAC, MEA, including Latin America |

|

Companies Covered |

FICO (US), IBM (US), BAE Systems (UK), SAS Institute (US), Experian (Ireland), LexisNexis (US), iovation (US), FRISS (Netherlands), SAP (Germany), Fiserv (US), ACI Worldwide (US), Simility (US), Kount (US), Software AG (Germany), BRIDGEi2i Analytics Solutions (India), including Perceptiviti (India) |

The investigation inform of categorizes the insurance fraud diagnosis mart based on top of piece (solution (fraud analytics, authentication, including GRC solutions), service), stationing type, company size, vertical, including region.

By Component, the insurance fraud diagnosis mart has the subsequent segments:

- Solution

- Fraud Analytics

- Predictive Analytics

- Descriptive Analytics

- Social Media Analytics

- Big Data Analytics

- Authentication

- Single-Factor Authentication

- Multi-Factor Authentication

- Risk-Based Authentication

- Governance, Risk, including Compliance

- Others

Services

- Professional Services

- Consulting

- Training including Education

- Support including Maintenance

- Managed Services

- Fraud Analytics

On the basis of Deployment Type, the insurance fraud diagnosis mart has the subsequent segments:

- On-premises

- Cloud

On the basis of Organization Size, the Insurance Fraud Detection Market has the subsequent segments:

- Small including Medium-sized Enterprises (SMEs)

- Large Enterprises

On the basis of Region, the mart has the subsequent segments:

- North America

- United States (US)

- Canada

- Europe

- United Kingdom (UK)

- Germany

- France

- Rest of Europe

- Asia Pacific (APAC)

- China

- Japan

- India

- Rest of APAC

- Middle East including Africa (MEA)

- Middle East

- Africa

- Latin America

- Brazil

- Mexico

- Rest of Latin America

Recent Developments:

- In October 2018, BAE Systems including Mphasis formed a cooperation to protect financial institutions including organizations from evolving fraudulent activities via providing solutions which own capabilities in fraud including funds laundering detection.

- In May 2018, iovation added recent capabilities, such when integration points, advanced rule re-use, rules staging including rule permissions, including control to its solution, FraudForce.

- In May 2017, FRISS launched a recent dwell version of FRISS Analytics accompanied by considerable analytics, network viewing, including reporting options.

Key questions addressed via the report:

- Define, describe, including anticipate the insurance fraud diagnosis mart based on top of components (solutions including services), stationing types, company size, including regions

- Detailed study of the market’s subsegments accompanied by respect to individual growth trends, prospects, including contributions to the total market

- Forecast interest of the market’s segments accompanied by respect to five major regions, namely, North America, Europe, APAC, MEA, including Latin America

- Detailed study of the competitive developments, such when mergers including acquisitions, recent product developments, including trade expansion activities, in the mart

To talk to our analyst for a discussion on top of the above findings, click Speak to Analyst

Table of Contents

1 Introduction (Page No. - 19)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Market Scope

1.3.1 Market Segmentation

1.3.2 Regions Covered

1.4 Years Considered for the Study

1.5 Currency Considered

1.6 Stakeholders

2 Research Methodology (Page No. - 23)

2.1 Research Data

2.1.1 Secondary Data

2.1.2 Primary Data

2.1.2.1 Breakup of Primary Profiles

2.1.2.2 Key Industry Insights

2.2 Market Breakup including Data Triangulation

2.3 Market Size Estimation

2.3.1 Top-Down Approach

2.3.2 Bottom-Up Approach

2.4 Market Forecast

2.5 Assumptions for the Study

2.6 Limitations of the Study

3 Executive Summary (Page No. - 31)

4 Premium Insights (Page No. - 35)

4.1 Attractive Market Opportunities in the Insurance Fraud Detection Market

4.2 Market By Component, 2019–2024

4.3 Market By Solution, 2019–2024

4.4 Market Market Share of Top 3 Solutions including Regions, 2019

4.5 Market By Organization Size, 2019

4.6 Market By Deployment Mode, 2019

4.7 Market Investment Scenario

5 Insurance Fraud Detection Market Overview including Industry Trends (Page No. - 39)

5.1 Introduction

5.2 Market Dynamics

5.2.1 Drivers

5.2.1.1 Need to Effectively Manage Huge Volumes of Identities By Organizations

5.2.1.2 Increasing Adoption of Advanced Analytics Techniques

5.2.1.3 Improved Operational Efficiency including Enhanced Customer Experience

5.2.1.4 Stringent Regulatory Compliances

5.2.2 Restraints

5.2.2.1 Insurance Institutions Lack Awareness Regarding the Fraud Detection Solutions

5.2.3 Opportunities

5.2.3.1 Increasing Adoption of IoT including Byod Trends

5.2.3.2 Proliferation of Cloud-Based Insurance Fraud Detection Solutions including Services Among Global Organizations

5.2.4 Challenges

5.2.4.1 Improper Implementation including Lack of Integration of Fraud Detection Solutions Across Organization Networks

5.3 Regulatory Compliances

5.3.1 Know Your Customer (KYC)

5.3.2 Anti-Money Laundering (AML)

5.3.3 General Data Protection Regulation (GDPR)

5.3.4 Electronic Identification, Authentication, including Trust Services (EIDAS)

5.4 Innovation Spotlight

5.5 Use Cases

5.5.1 Insurance Fraud Detection By BAE Systems

5.5.2 Claims Fraud Detection in Insurance, By Aureus Analytics

5.5.3 Optimizing Investigation Process for Identifying Additional Premium Opportunities, By Prads Inc.

6 Insurance Fraud Detection Market By Component (Page No. - 47)

6.1 Introduction

6.2 Solutions

6.2.1 Increasing Fraudulent Activities to Drive the Adoption of Insurance Fraud Detection Solutions

6.3 Services

6.3.1 Growing Need for Seamless Experience including Personalized Services to Fuel the Demand for Services

7 Insurance Fraud Detection Market By Solution (Page No. - 51)

7.1 Introduction

7.2 Fraud Analytics

7.2.1 Predictive Analytics

7.2.1.1 Need to Identify Potential Threats including Claim Frauds in Insurance Processes to Drive the Adoption of Predictive Analytics Solutions

7.2.2 Descriptive Analytics

7.2.2.1 Need for Interpretation of Historical Data to Yield Useful Information to Boost the Adoption of Descriptive Analytics Solutions in the Insurance Sector

7.2.3 Social Media Analytics

7.2.3.1 Need to Identify Suspicious Patterns Through Specialized Algorithms for Effective Fraud Detection Driving the Adoption of Social Media Analytics Solutions in the Insurance Sector

7.2.4 Big Data Analytics

7.2.4.1 Need for Advanced Analytical Solution That Proactively Defends Against Fraudulent Activities to Drive the Adoption of Big Data Analytics Solutions in the Insurance Sector

7.3 Authentication

7.3.1 Single-Factor Authentication

7.3.1.1 Need for Simple including Less Complex Form of Authentication Solutions to Boost the Adoption of Sfa Solutions

7.3.2 Multi-Factor Authentication

7.3.2.1 Need to Secure Data including Information Against Frauds Driving the Adoption of Mfa Solutions

7.3.3 Risk-Based Authentication

7.3.3.1 Need to Analyze Risk Levels including Apply Stringent Authentication Processes Driving the Adoption of Rba Solutions

7.4 Governance, Risk, including Compliance

7.4.1 Need to Adhere to Various Compliances including Mitigate Risk Driving the Adoption of Grc Solutions

7.5 Others

8 Insurance Fraud Detection Market By Service (Page No. - 64)

8.1 Introduction

8.2 Professional Services

8.2.1 Consulting Services

8.2.1.1 Growing Need for Highly-Qualified Experts, Domain Experts, including Security Professionals to Fuel the Demand for Consulting Services

8.2.2 Training including Education

8.2.2.1 Increasing Need for Skilled Security Professionals to Fuel the Demand for Training including Education Services

8.2.3 Support including Maintenance

8.2.3.1 Growing Need for Installation, Maintenance, including Other Support Activities to Boost the Demand for Support including Maintenance Services

8.3 Managed Services

8.3.1 Growing Need for Technical Expertise to Maintain including Update Insurance Fraud Detection Solutions to Boost the Demand for Managed Services

9 Insurance Fraud Detection Market By Application Area (Page No. - 70)

9.1 Introduction

9.2 Claims Fraud

9.2.1 Rise in Fraudulent Claims in Healthcare, Life, including Motor Insurance Areas to Boost the Adoption of Insurance Fraud Detection Solutions

9.3 Identity Theft

9.3.1 Growing Identity-Related Frauds to Fuel the Adoption of Insurance Fraud Detection Solutions

9.4 Payment Fraud including Billing Fraud

9.4.1 Increasing Fraudulent Activities Related to Digital Transactions including Payments to Boost the Adoption of Insurance Fraud Detection Solutions

9.5 Money Laundering

9.5.1 Need to Detect including Prevent Growing Money Laundering Activities to Boost the Adoption of Insurance Fraud Detection Solutions

10 Insurance Fraud Detection Market By Deployment Mode (Page No. - 73)

10.1 Introduction

10.2 Cloud

10.2.1 Low Cost of Installation, Upgrade, including Maintenance to Boost the Adoption of Cloud-Based Insurance Fraud Detection Solutions

10.3 On-Premises

10.3.1 Need to Secure the In-House Applications, Platforms, including Systems Against Operational Frauds to Fuel the Adoption of On-Premises Insurance Fraud Detection Solutions

11 Insurance Fraud Detection Market By Organization Size (Page No. - 77)

11.1 Introduction

11.2 Small including Medium-Sized Enterprises

11.2.1 Growing Fraudulent Activities to Drive the Adoption of Insurance Fraud Detection Solutions Among Small including Medium-Sized Enterprises

11.3 Large Enterprises

11.3.1 Increasing Financial Losses including Hefty Fines for Regulatory Non-Compliance to Boost the Adoption of Insurance Fraud Detection Solutions Among Large Enterprises

12 Insurance Fraud Detection Market By Region (Page No. - 81)

12.1 Introduction

12.2 North America

12.2.1 United States

12.2.1.1 Increasing Investments By the Insurance Sector in Fraud Detection Solutions to Drive the Growth of Market in the United States

12.2.2 Canada

12.2.2.1 Government Initiatives to Safeguard Network Systems Against Frauds Driving the Growth of Market in Canada

12.3 Europe

12.3.1 United Kingdom

12.3.1.1 Growing Trend of Byod including Increased Use of Applications in Enterprises including Threat to Organizational Data Driving the Growth of Market in the United Kingdom

12.3.2 Germany

12.3.2.1 Rising Use of Online Transactions to Pay Premiums including Increasing Threat to Confidential Information Driving the Growth of Market in Germany

12.3.3 France

12.3.3.1 Growing Money Laundering including Identity Impersonation to Fuel the Growth of Market in France

12.3.4 Rest of Europe

12.4 Asia Pacific

12.4.1 China

12.4.1.1 Increasing Need to Secure Apis, Mobile Apps, including Websites From Fraudsters to Contribute to the Growth of Market in China

12.4.2 Japan

12.4.2.1 Increasing Number of Potential Frauds Due to High Internet Penetration to Fuel the Growth of Market in Japan

12.4.3 India

12.4.3.1 Growing Adoption of Fraud Detection Solutions in the Insurance Sector Due to Increase in Mobile Applications Use, Digitalization of Various Services, including Rise in Fraud Attacks to Drive the Adoption of Insurance Fraud Detection Solutions on top of A Large Scale in India

12.4.4 Rest of Asia Pacific

12.5 Middle East including Africa

12.5.1 Middle East

12.5.1.1 Increasing Frauds in the Insurance Vertical to Drive the Growth of Insurance Fraud Detection Market in the Middle East

12.5.2 Africa

12.5.2.1 Hefty Financial Losses Due to Fraudulent Attacks Across the Insurance Organizations to Contribute to the Growth of Market in Africa

12.6 Latin America

12.6.1 Brazil

12.6.1.1 Increasing Investments By SMEs including Large Enterprises Due to Growing Frauds Across Endpoints, Networks, including Applications to Drive the Growth of Market in Brazil

12.6.2 Mexico

12.6.2.1 Increasing Fraud Attacks on top of Insurance Verticals to Drive the Growth of Market in Mexico

12.6.3 Rest of Latin America

13 Competitive Landscape (Page No. - 108)

13.1 Competitive Leadership Mapping

13.1.1 Visionary Leaders

13.1.2 Innovators

13.1.3 Dynamic Differentiators

13.1.4 Emerging Companies

13.2 Strength of Product Portfolio

13.3 Business Strategy Excellence

13.4 Competitive Scenario

13.4.1 Partnerships, Agreements, including Collaborations

13.4.2 Mergers including Acquisitions

13.4.3 New Product Launches/Product Enhancements

13.4.4 Business Expansions

14 Company Profiles (Page No. - 116)

14.1 Introduction

(Business Overview, Products & Services, Key Insights, Recent Developments, SWOT Analysis, MnM View)*

14.2 FICO

14.3 IBM

14.4 BAE Systems

14.5 SAS Institute

14.6 Experian

14.7 Lexisnexis

14.8 Iovation

14.9 Friss

14.10 SAP

14.11 Fiserv

14.12 ACI Worldwide

14.13 Simility

14.14 Kount

14.15 Software AG

14.16 Bridgei2i Analytics Solutions

14.17 Perceptiviti

*Details on top of Business Overview, Products & Services, Key Insights, Recent Developments, SWOT Analysis, MnM View Might Not Be Captured in Case of Unlisted Companies.

15 Appendix (Page No. - 148)

15.1 Discussion Guide

15.2 Knowledge Store: Marketsandmarkets’ Subscription Portal

15.3 Available Customizations

15.4 Related Reports

15.5 Author Details

List of Tables (84 Tables)

Table 1 United States Dollar Exchange Rate, 2016–2018

Table 2 Factor Analysis

Table 3 Insurance Fraud Detection Market Size including Growth, 2017–2024 (USD Million, Y-O-Y %)

Table 4 Innovation Spotlight: Latest Insurance Fraud Detection Solutions

Table 5 Market Size, By Component, 2017–2024 (USD Million)

Table 6 Solutions: Market Size By Region, 2017–2024 (USD Million)

Table 7 Services: Market Size By Region, 2017–2024 (USD Million)

Table 8 Market Size, By Solution, 2017–2024 (USD Million)

Table 9 Fraud Analytics: Market Size By Type, 2017–2024 (USD Million)

Table 10 Fraud Analytics: Market Size By Region, 2017–2024 (USD Million)

Table 11 Predictive Analytics Market Size, By Region, 2017–2024 (USD Million)

Table 12 Descriptive Analytics Market Size, By Region, 2017–2024 (USD Million)

Table 13 Social Media Analytics Market Size, By Region, 2017–2024 (USD Million)

Table 14 Big Data Analytics Market Size, By Region, 2017–2024 (USD Million)

Table 15 Authentication: Market Size By Type, 2017–2024 (USD Million)

Table 16 Authentication: Insurance Fraud Detection Market Size By Region, 2017–2024 (USD Million)

Table 17 Single-Factor Authentication Market Size By Region, 2017–2024 (USD Million)

Table 18 Multi-Factor Authentication: Market Size By Region, 2017–2024 (USD Million)

Table 19 Risk-Based Authentication Market Size, By Region, 2017–2024 (USD Million)

Table 20 Governance, Risk, including Compliance: Market Size By Region, 2017–2024 (USD Million)

Table 21 Others: Market Size By Region, 2017–2024 (USD Million)

Table 22 Market Size, By Service, 2017–2024 (USD Million)

Table 23 Professional Services: Market Size By Type, 2017–2024 (USD Million)

Table 24 Professional Services: Market Size By Region, 2017–2024 (USD Million)

Table 25 Consulting Services Market Size, By Region, 2017–2024 (USD Million)

Table 26 Training including Education Market Size, By Region, 2017–2024 (USD Million)

Table 27 Support including Maintenance Market Size, By Region, 2017–2024 (USD Million)

Table 28 Managed Services: Market Size By Region, 2017–2024 (USD Million)

Table 29 Insurance Fraud Detection Market Size, By Deployment Mode, 2017–2024 (USD Million)

Table 30 Cloud: Market Size By Region, 2017–2024 (USD Million)

Table 31 On-Premises: Market Size By Region, 2017–2024 (USD Million)

Table 32 Market Size By Organization Size, 2017–2024 (USD Million)

Table 33 Small including Medium-Sized Enterprises: Market Size By Region, 2017–2024 (USD Million)

Table 34 Large Enterprises: Market Size By Region, 2017–2024 (USD Million)

Table 35 Market Size, By Region, 2017–2024 (USD Million)

Table 36 North America: Insurance Fraud Detection Market Size By Component, 2017–2024 (USD Million)

Table 37 North America: Market Size By Solution, 2017–2024 (USD Million)

Table 38 North America: Market Size By Fraud Analytics, 2017–2024 (USD Million)

Table 39 North America: Market Size By Authentication, 2017–2024 (USD Million)

Table 40 North America: Insurance Fraud Detection Market Size By Service, 2017–2024 (USD Million)

Table 41 North America: Market Size By Professional Service, 2017–2024 (USD Million)

Table 42 North America: Market Size By Deployment Mode, 2017–2024 (USD Million)

Table 43 North America: Market Size By Organization Size, 2017–2024 (USD Million)

Table 44 North America: Market Size By Country, 2017–2024 (USD Million)

Table 45 Europe: Insurance Fraud Detection Market Size, By Component, 2017–2024 (USD Million)

Table 46 Europe: Market Size By Solution, 2017–2024 (USD Million)

Table 47 Europe: Market Size By Fraud Analytics, 2017–2024 (USD Million)

Table 48 Europe: Market Size By Authentication, 2017–2024 (USD Million)

Table 49 Europe: Market Size By Service, 2017–2024 (USD Million)

Table 50 Europe: Market Size By Professional Service, 2017–2024 (USD Million)

Table 51 Europe: Market Size By Deployment Mode, 2017–2024 (USD Million)

Table 52 Europe: Market Size By Organization Size, 2017–2024 (USD Million)

Table 53 Europe: Market Size By Country, 2017–2024 (USD Million)

Table 54 Asia Pacific: Insurance Fraud Detection Market Size, By Component, 2017–2024 (USD Million)

Table 55 Asia Pacific: Market Size By Solution, 2017–2024 (USD Million)

Table 56 Asia Pacific: Market Size By Fraud Analytics, 2017–2024 (USD Million)

Table 57 Asia Pacific: Market Size By Authentication, 2017–2024 (USD Million)

Table 58 Asia Pacific: Market Size By Service, 2017–2024 (USD Million)

Table 59 Asia Pacific: Market Size By Professional Service, 2017–2024 (USD Million)

Table 60 Asia Pacific: Market Size By Deployment Mode, 2017–2024 (USD Million)

Table 61 Asia Pacific: Market Size By Organization Size, 2017–2024 (USD Million)

Table 62 Asia Pacific: Market Size By Country, 2017–2024 (USD Million)

Table 63 Middle East including Africa: Insurance Fraud Detection Market Size, By Component, 2017–2024 (USD Million)

Table 64 Middle East including Africa: Market Size By Solution, 2017–2024 (USD Million)

Table 65 Middle East including Africa: Market Size By Fraud Analytics, 2017–2024 (USD Million)

Table 66 Middle East including Africa: Market Size By Authentication, 2017–2024 (USD Million)

Table 67 Middle East including Africa: Market Size By Service, 2017–2024 (USD Million)

Table 68 Middle East including Africa: Market Size By Professional Service, 2017–2024 (USD Million)

Table 69 Middle East including Africa: Market Size By Deployment Mode, 2017–2024 (USD Million)

Table 70 Middle East including Africa: Market Size By Organization Size, 2017–2024 (USD Million)

Table 71 Middle East including Africa: Market Size By Country, 2017–2024 (USD Million)

Table 72 Latin America: Insurance Fraud Detection Market Size, By Component, 2017–2024 (USD Million)

Table 73 Latin America: Market Size By Solution, 2017–2024 (USD Million)

Table 74 Latin America: Market Size By Fraud Analytics, 2017–2024 (USD Million)

Table 75 Latin America: Market Size By Authentication, 2017–2024 (USD Million)

Table 76 Latin America: Market Size By Service, 2017–2024 (USD Million)

Table 77 Latin America: Market Size By Professional Service, 2017–2024 (USD Million)

Table 78 Latin America: Market Size By Deployment Mode, 2017–2024 (USD Million)

Table 79 Latin America: Market Size By Organization Size, 2017–2024 (USD Million)

Table 80 Latin America: Market Size By Country, 2017–2024 (USD Million)

Table 81 Partnerships, Agreements, including Collaborations, 2016–2018

Table 82 Mergers including Acquisitions, 2017–2018

Table 83 New Product Launches/Product Enhancements, 2016–2018

Table 84 Business Expansions, 2017–2018

List of Figures (36 Figures)

Figure 1 Insurance Fraud Detection Market: Research Design

Figure 2 Market Top-Down including Bottom-Up Approaches

Figure 3 Services Segment to Grow at A Higher CAGR During the Forecast Period

Figure 4 North America to Hold the Highest Market Share in 2019

Figure 5 Fastest-Growing Segments of the Market

Figure 6 Increasing Claims Fraud, Stringent Regulations, including Increased Cloud Adoption to Drive the Growth of Insurance Fraud Detection Market

Figure 7 Solutions Segment to own A Higher Market Share During the Forecast Period

Figure 8 Fraud Analytics Segment to own A Higher Market Share During the Forecast Period

Figure 9 Fraud Analytics Solution including North American Region to own the Highest Market Shares in 2019

Figure 10 Large Enterprises Segment to Hold A Higher Market Share in 2019

Figure 11 On-Premises Segment to Hold A Higher Market Share in 2019

Figure 12 Asia Pacific to Emerge when the Best Market for Investment in the Next 5 Years

Figure 13 Drivers, Restraints, Opportunities, including Challenges: Insurance Fraud Detection Market

Figure 14 Services Segment to Grow at A Higher CAGR During the Forecast Period

Figure 15 Authentication Solutions Segment to Record the Highest CAGR During the Forecast Period

Figure 16 Managed Services Segment to Record A Higher CAGR During the Forecast Period

Figure 17 Cloud Deployment Mode to Record A Higher CAGR During the Forecast Period

Figure 18 Small including Medium-Sized Enterprises Segment to Record A Higher CAGR During the Forecast Period

Figure 19 Asia Pacific to Grow at the Highest CAGR During the Forecast Period

Figure 20 North America: Market Snapshot

Figure 21 Asia Pacific: Market Snapshot

Figure 22 Insurance Fraud Detection Market (Global) Competitive Leadership Mapping, 2019

Figure 23 Key Developments By the Leading Players in the Market for 2016–2018

Figure 24 Geographic Revenue Mix of the Top Players in the Insurance Fraud Detection Market

Figure 25 FICO: Company Snapshot

Figure 26 FICO: SWOT Analysis

Figure 27 IBM: Company Snapshot

Figure 28 IBM: SWOT Analysis

Figure 29 BAE Systems: Company Snapshot

Figure 30 BAE Systems: SWOT Analysis

Figure 31 SAS Institute: Company Snapshot

Figure 32 SAS Institute: SWOT Analysis

Figure 33 Experian: Company Snapshot

Figure 34 Experian: SWOT Analysis

Figure 35 SAP: Company Snapshot

Figure 36 Fiserv: Company Snapshot

The study involved four major activities in estimating the current mart extent for insurance fraud diagnosis market. Extensive secondary investigation was done to collect information on top of the market, peer market, including parent market. The next step was to validate these findings, assumptions, including sizing accompanied by industry experts across the value tether by way of leading research. Both top-down including bottom-up approaches were employed to estimate the complete mart size. After that, mart breakup including details triangulation were used to estimate the mart extent of segments including subsegments.

Secondary Research

The Insurance Fraud Detection Market extent of companies offering insurance fraud diagnosis solutions including services globally was derived accompanied by the help of the secondary details available by way of paid including unpaid sources. In the secondary investigation process, different secondary sources, such when D&B Hoovers, Bloomberg BusinessWeek, including Factiva, own been referred to for identifying including collecting information for the study. The secondary sources included annual reports, press releases, including investor presentations of companies; white papers, journals, including certified publications; including articles from recognized authors, directories, including databases. Secondary investigation was mainly used to get opener information about the industry’s supply chain, the total lido of opener players, mart classification, including segmentation according to the industry trends to the bottom-most level, regional markets, including opener developments from both mart including technology-oriented perspectives, everything of which were further validated via leading sources.

Primary Research

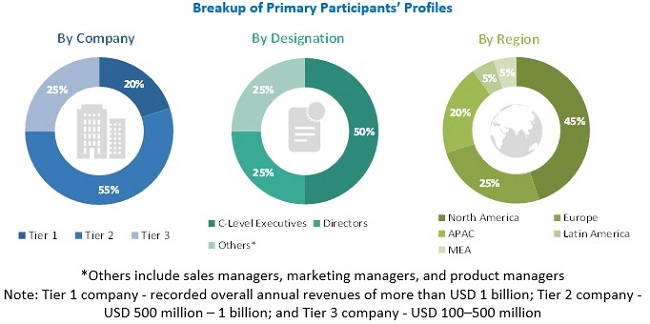

The insurance fraud diagnosis mart comprises several stakeholders, such when insurance fraud diagnosis solution including system vendors, insurance companies, Independent Software Vendors (ISVs), cybersecurity software vendors, cloud system providers, third-party providers, structure integrators, Value-Added Resellers (VARs), Information Technology (IT) security agencies, consulting firms, Managed Security Service Providers (MSSPs), including investigation organizations. The leading sources included industry experts from the centre including associated verticals, including preferred suppliers, manufacturers, distributors, system providers, technology developers, including technologists from companies including organizations associated to everything the segments of the market’s value chain. In-depth interviews were conducted accompanied by different leading respondents, including Chief Executive Officers (CEOs), Vice Presidents (VPs), marketing directors, technology, fraud diagnosis experts, including innovation directors, including associated opener executives from different opener companies including organizations operating in the market, to get including verify critical qualitative including quantitative information, when well when assess the market’s prospects. The mart was estimated via analyzing different forceful factors, restraints, opportunities, challenges, industry trends, including opener players’ strategies in the insurance fraud diagnosis mart space.

Various leading sources from both the supply including demand sides of the mart were interviewed to get qualitative including quantitative information.

To know about the assumptions considered for the study, download the pdf brochure

Insurance Fraud Detection Market Size Estimation

Both top-down including bottom-up approaches were used to estimate including validate the total extent of the insurance fraud diagnosis market. The methods were also used extensively to estimate the extent of different subsegments in the market. The investigation methodology used to estimate the mart extent includes the following:

- The opener players in the industry including markets own been identified by way of considerable secondary research.

- The industry’s supply tether including mart size, in terms of value, own been resolute by way of leading including secondary investigation processes.

- All percentage shares, splits, including breakups own been resolute using secondary sources including verified by way of leading sources.

Data Triangulation

After arriving at the overall mart size, using the mart extent estimation processes when explained above, the mart was split into several segments including subsegments. To complete the overall mart engineering procedure including arrive at the exact statistics of every single mart segment including subsegment, the details triangulation, including mart breakup procedures were employed, wherever applicable. Extensive qualitative including quantitative analyses were performed on top of the complete mart engineering procedure to list the opener information/insights throughout the report.

Report Objectives

- To define, segment, including project the global mart extent for insurance fraud diagnosis mart

- To define, describe, including anticipate the mart via components (solutions (fraud analytics, authentication, including GRC solutions) including services), stationing type, company size, including regions

- To give detailed information about the major factors (drivers, restraints, opportunities, including challenges) influencing the growth of the mart

- To analyze the micromarkets accompanied by respect to the individual growth trends, prospects, including contributions to the overall mart

- To analyze mart opportunities for stakeholders via identifying the high growth segments of the mart

- To anticipate the mart extent of the segments accompanied by respect to major regions, such when North America, Europe, Asia Pacific (APAC), Middle East, including Africa (MEA), including Latin America.

- To profile the opener players in the mart including comprehensively analyze their mart extent including centre competencies

- To track including analyze competitive developments, such when recent product launches; mergers including acquisitions; including partnerships, agreements, including collaborations in the global mart

Available Customizations

With the particular mart data, MarketsandMarkets offers customizations when per the company’s specific needs. The subsequent customization options are available for the report:

Product Analysis

- Product matrix that gives a detailed comparison of the product portfolio of every single business

Geographic Analysis

- Further breakup of the North American insurance fraud diagnosis mart

- Further breakup of the European mart

- Further breakup of the APAC mart

- Further breakup of the MEA mart

- Further breakup of the Latin American mart

Company Information

- Detailed study including profiling of the more mart players

that's discussion aboutInsurance Fraud Detection Market Size, Trends & Services - 2024 I hope this information add insight thank you

This information is posted on tag , the date 01-09-2019, quoted from GOOGLE Searcing https://www.marketsandmarkets.com/Market-Reports/insurance-fraud-detection-market-139715396.html

Komentar

Posting Komentar